April Intown Atlanta Market Report

By Bill Adams, President

The first quarter of 2026 is in the rearview mirror, and we will attempt to assess the state of the Intown Atlanta single-family residential real estate market at the end of the quarter. First, let’s look at the overall market.

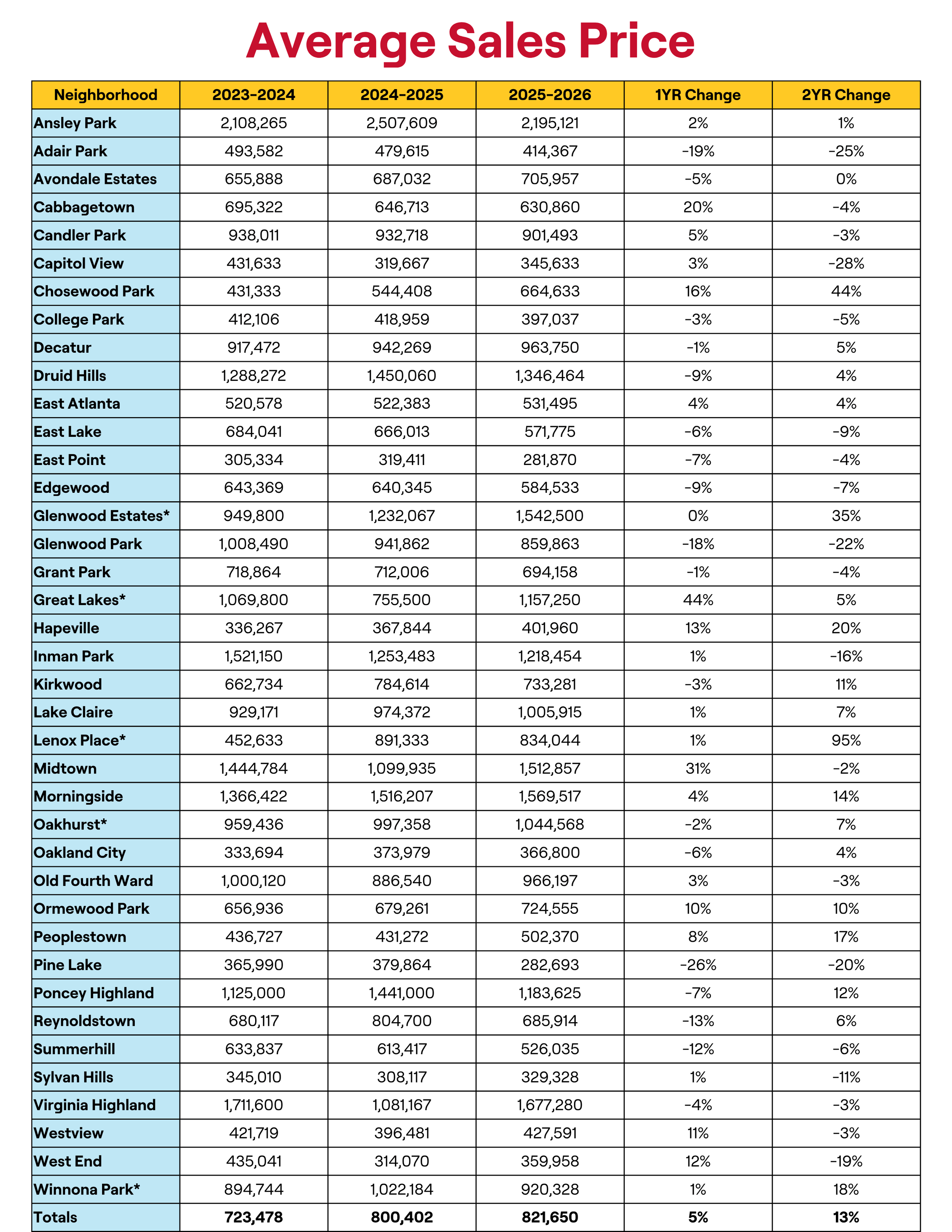

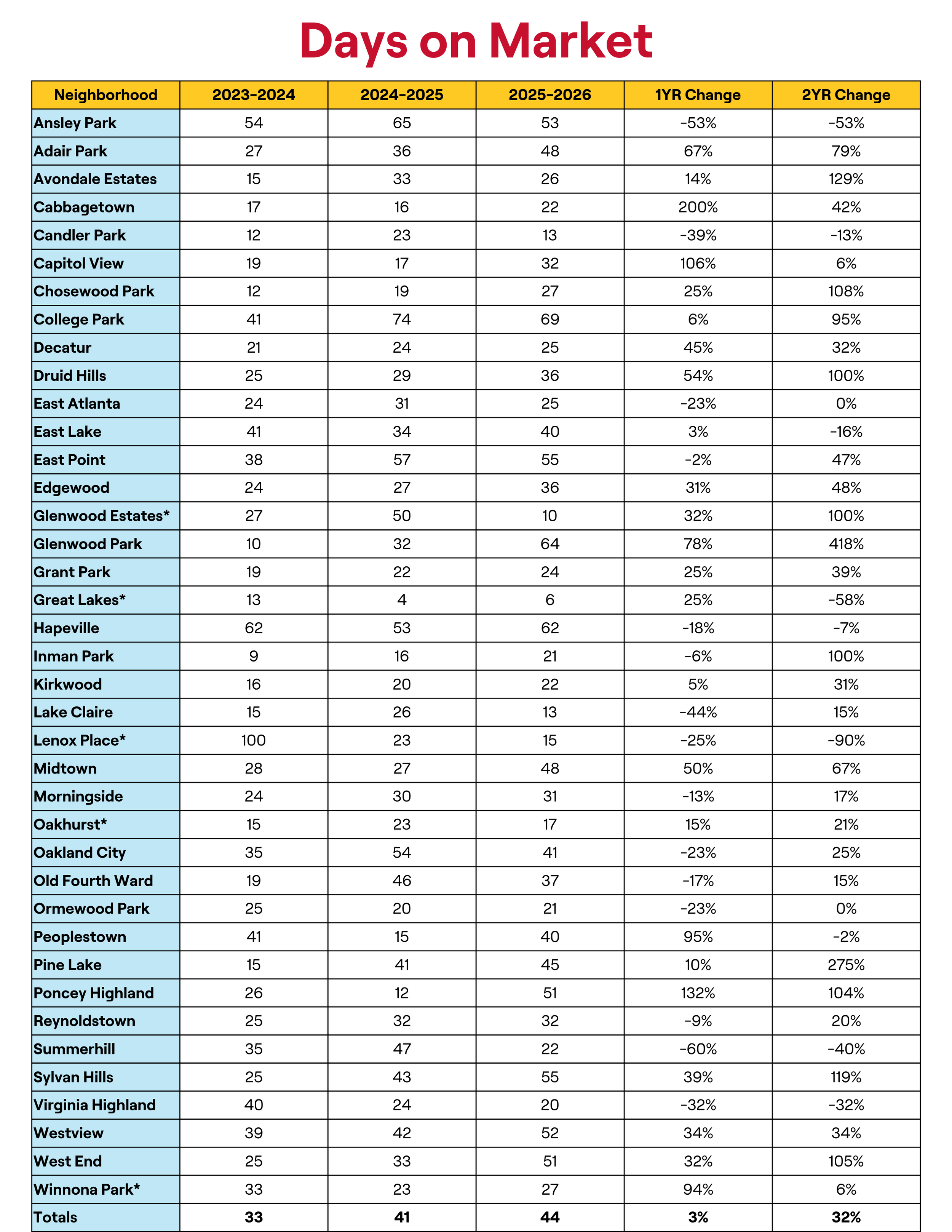

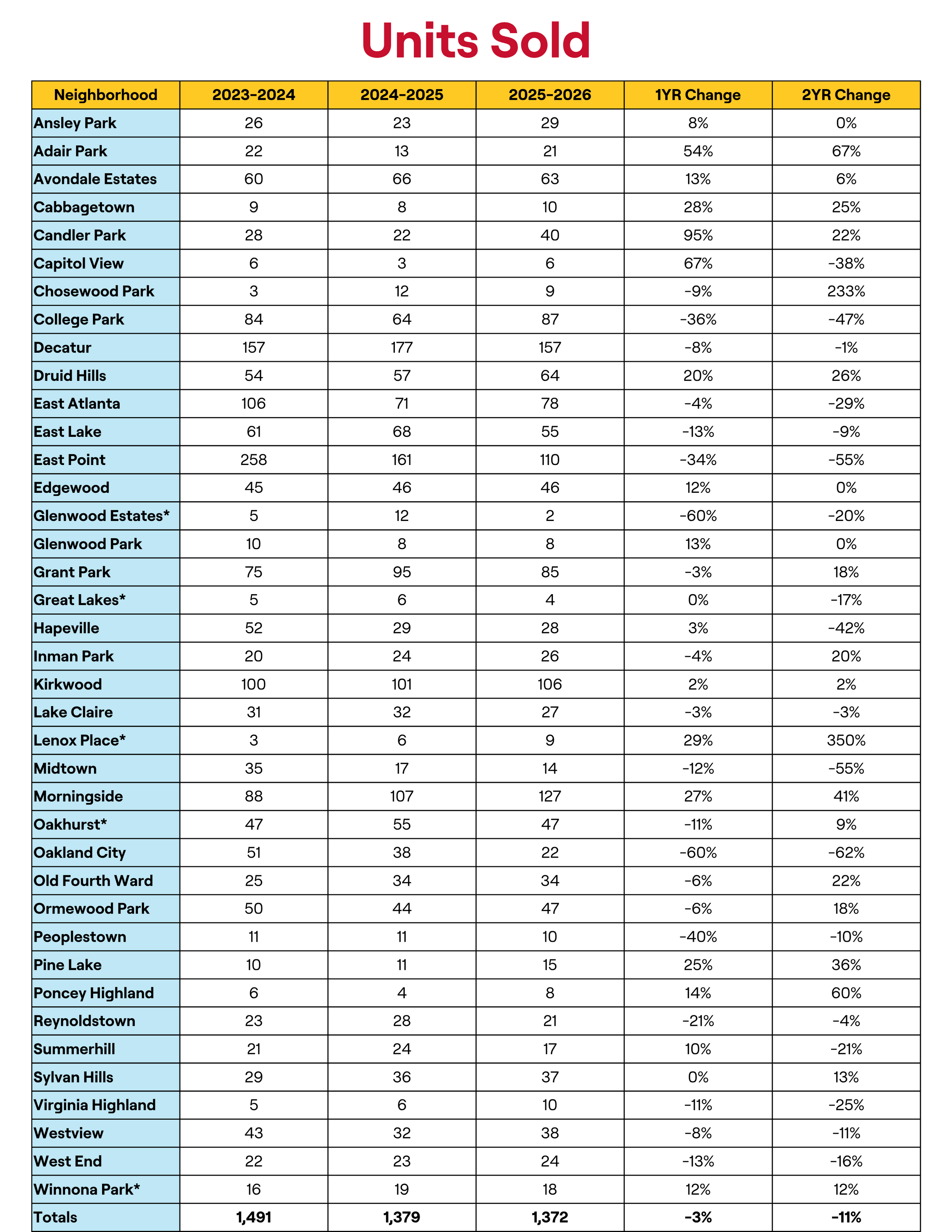

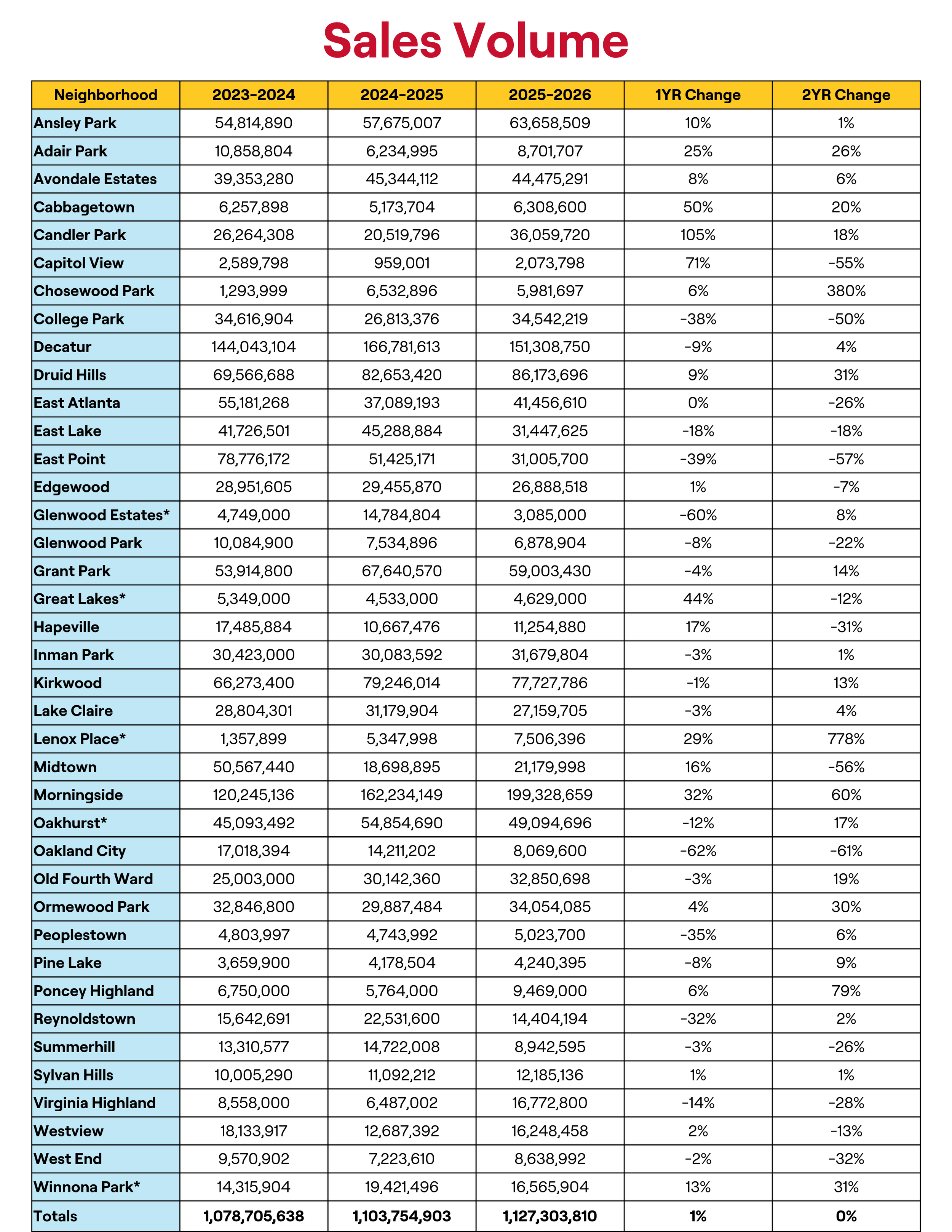

This month, the Average Sales Price (ASP) is $821,650, a 3% year-over-year increase and a 14% increase over the past two years. However, April’s ASP is about 1.5% lower than March’s figure of $833,241. The average number of days on the market is now 44 days, an increase of 6% over the last year and a 32% increase over the past 24 months. In the past year, 1,372 homes sold, a 1% decrease from the previous year and an 8% decrease compared to two years ago. For the first time since 2010, a slight majority (20 out of the 39 markets we survey) experienced a decrease in Average Sales Price over the last 12 months. Taken together, these numbers point to some weakness in the Intown market.

In December 2025, I predicted that home mortgage rates would track in a narrow band around 6%. Mortgage rates are currently around 6.48%. I also expected prices to increase by 5% this year; however, the Average Sales Price is currently up 3% and declining in many markets. I predicted that the average days on market would rise to the mid-40s, and as noted above, the current average is 44 days.

Let me be clear—the housing market is not what it was in 2010, and we are not revisiting the Great Recession. The softness in the Intown market is a trend that has been building over the last few years. Last April, for example, 16 markets were already in negative Average Sales Price territory. I believe there are two primary causes of the current softening.

First, prices in some markets may have reached a ceiling. The market is elastic, not inelastic, and there is a limit to how much prices can increase. Second, uncertainty surrounding foreign and domestic policy at the federal level can impact mortgage interest rates, as investor confidence in Treasury notes fluctuate—ultimately influencing borrowing costs. Additionally, prospective homebuyers may hesitate to commit to a purchase amid concerns about job security and the potential for a recession.

Next month, we will revisit the communities adjacent to the Atlanta BeltLine, beginning with the Northeast segment.